Market intelligence firm CONTEXT has outlined a rise in Chinese metal 3D printer shipments in Q1 2024.

This trend, also evident in CONTEXT’s Q4 2023 report, continued amid stagnating global industrial polymer 3D printer performance. Vat Photopolymerization system sales were particularly weak, heavily contributing to the -15% YoY decline in the Industrial price class.

The shift toward entry-level FDM 3D printers, especially those offered by Bambu Lab, continued into 2024. Professional users continue to recognize that 3D printers in the sub-$2500 price range now offer the features and functionality of more costly models.

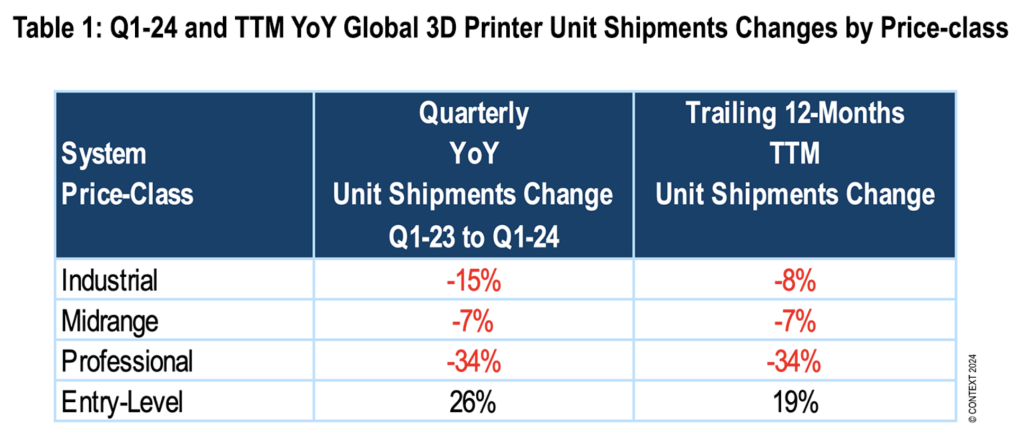

This caused global shipments of entry-level 3D printers to increase 26% YoY, while Midrange and Professional offerings fell by 7% and 34%, respectively.

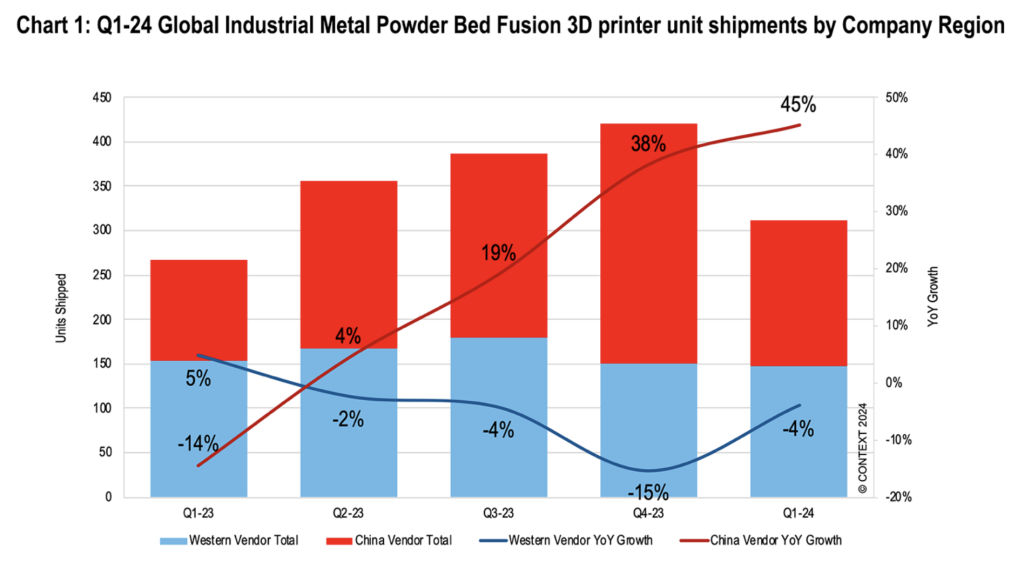

In Q1’24, Chinese vendors were reportedly elated by strong domestic demand, especially within the Industrial Metal Powder Bed Fusion space, witnessing 45% growth in metal powder bed fusion (PBF) systems. Alternatively, Western vendors continued to experience end–market challenges associated with low Capital Expenditure due to “high interest rates and sticky inflation.”

US and European vendors did report strong demand from defense markets in Q1 2024, amid efforts to create more resilient localized supply chains.

Polymer 3D printers face falling shipments

Industrial 3D printers performed poorly in Q1 2024. Global shipments fell by 15% YoY, down 8% on a trailing twelve-month basis. Weak sales of Industrial Polymer 3D printers, which accounted for 50% of the category’s total shipments, significantly contributed to these poor results.

29% fewer Industrial polymer 3D printers were shipped in Q1’24 than Q1’23, with Industrial Vat Photopolymerization systems down by 47% YoY. According to CONTEXT, the decline was driven by weak shipments from the two leading regional companies in this sector: UnionTech in China and 3D Systems in the US.

Notably, nine of this sector’s top ten global companies saw polymer 3D printer shipments fall compared to the previous year. Most saw shipments decrease by double-digit percentage points.

When Vat Photopolymerization 3D printers are excluded, shipments fell by only 1% YoY. This drop was mainly driven by weak performance in the global dental market, with high inflation creating a shift in end–market demand for cosmetic dentistry.

China continues Industrial metal 3D printer domination

Industrial metal 3D printers continued to perform well in Q1 2024. Shipments increased by 10% worldwide, up 4% on a trailing twelve-month basis.

PBF systems dominated the metal additive manufacturing market, accounting for the largest proportion (74%) of printers in the category – up 7% YoY. All other metal 3D printing systems, except material jetting, also posted yearly shipments growth. Directed Energy Deposition shipments were up 21%, Material Extrusion 3D printers increased by 32%, and Binder Jetting adoption was up 15%.

China has spearheaded the demand for PBF systems, with 3D printer shipments from Chinese vendors increasing by 45%. Conversely, Western metal PBF 3D printer OEMs saw shipments decrease by 4%.

Moreover, Chinese firms have achieved shipment growth in the last four consecutive quarters. Western vendors, on the other hand, have posted four consecutive quarters of declining shipments.

The four companies that shipped the most metal Powder Bed Fusion 3D printers in Q1 2024 were Chinese, Xi’an Bright Laser Technologies, ZRapid Tech, Farsoon Technologies, and Eplus3D. The latter reportedly topped the industry in terms of unit shipments.

Western metal 3D printer manufacturers led the industry in terms of System Revenue contribution. German-based Nikon SLM Solutions and EOS enjoyed the top market share positions in metal PBF revenue. Nikon SLM was notable as a leader in large-scale, multi-laser 3D printers.

A “transition period” for Midrange and Professional 3D printers

Shipments of Midrange 3D printers costing between $20-100K fell by 7% in Q1 2024, mostly driven by declining Polymer Powder Bed Fusion 3D printers, which fell 14% YoY.

Demand in this price class was poor globally, with shipments from Chinese companies falling by 1% YoY. Western vendors saw shipments decrease by 9% in Q1’24. In fact, of the top five vendors in this area, China’s ZRapid Tech was the only firm to experience YoY growth. The company experienced strength in its SLA Vat Photopolymerization and low–end Metal Powder Bed Fusion line.

The other leading top-five Midrange firms, Stratasys, UnionTech, Formlabs and 3D Systems, saw YoY shipment decline in this area.

The market for Professional 3D printers costing between $2.5 and $20K continued to perform poorly, with 34% fewer products shipped globally in Q1’24. This marked the eighth consecutive period of YoY shipment decline, as entry-level 3D printers cannibalize a growing portion of their purchasing base. Of the top ten OEMs, all but two saw shipments fall.

CONTEXT called Q1 2024 a transition period as the two price-class leaders, Formlabs and UltiMaker, introduced new products. The latter continued to extend its portfolio into a higher price point with its new Factor 4 3D printer. Formlabs launched the Form 4, a new vat photopolymerization 3D printer which follows its traditional pricing strategy.

The entry-level 3D printer boom continues

Shipments of sub-$2,500 entry-level 3D printers continued to accelerate in 2024, up 26% from Q1 2023. Efforts to accelerate the use of these low-cost 3D printers in more professional end markets, including on print farms, continued to help the market segment soar.

Nine of the top ten manufacturers in this space saw more 3D printers ship in this period than the previous year. CONTEXT called Bambu Lab the industry leader whose growth was the most impressive.

Fellow Shenzhen-based company Creality also remained a dominant force in this price range, accounting for 56% of all entry-level 3D printer shipments in Q1’24. Anycubic reportedly fell far behind these two industry leaders. Excluding Creality and Bambu Lab, shipments increased modestly by 9%.

The market success of Bambu’s AMS (Automatic Material System) multi-color 3D printing technology saw many vendors introduce similar products in Q1 2024.

The US remained the leading end market for entry-level 3D printer shipments, accounting for 42% of the units shipped globally during this period. Approximately 94% of all shipped entry-level 3D printers came from Chinese companies.

Take 10 seconds to tell us the impact of this news using the block below. Make sure you click submit!

CONTEXT reports mixed 3D printing outlook

Industry consolidation dominated discourse in the West during Q1’24. This was driven by Nano Dimension’s planned acquisition of Desktop Metal, announced in July 2024.

Merger and acquisition rumors persist in the US and Europe, with several publicly traded companies under strategic review. Chinese companies, however, continue to thrive domestically while expanding their overseas businesses.

In the West, forecasts remain largely conservative. However, strong Chinese demand for Metal Powder Bed Fusion 3D printers has led to a revised global industrial printer shipment forecast, which now projects a 7% increase by the end of the year. The demand companies like Nexa3D and Velo3D are experiencing from the defense sector has supported this increase.

The Midrange category forecast now sits at a modest 3% YoY growth, while Professional 3D printer shipments are expected to decline by 1%. CONTEXT expects entry-level growth to continue, projecting a 14% rise driven by the new market options unlocked through Bambu Lab’s success.

Accelerated growth for Industrial systems is anticipated in 2025 and beyond, as the US and Europe stabilize following post-election cycles and interest rates drop. 3D printing manufacturers are expected to continue their efforts to expand additive technology into mainstream manufacturing. However, many strategic initiaitves are also starting to incorporate other digital technologies beyond 3D printing into their portfolios to accelerate growth.

Nominations are now open for the 2024 3D Printing Industry Awards.

What does the future of 3D printing hold?

What near-term 3D printing trends have been highlighted by industry experts?

Subscribe to the 3D Printing Industry newsletter to keep up with the latest 3D printing news.

You can also follow us on Twitter, like our Facebook page, and subscribe to the 3D Printing Industry Youtube channel to access more exclusive content.

Featured image shows Q1’24 global Industrial Metal Powder Bed Fusion 3D printer unit shipments by company region. Image via CONTEXT.