Speaker

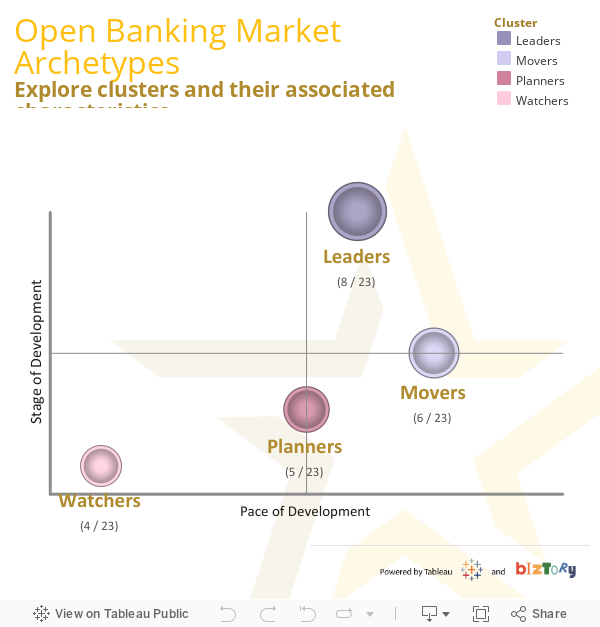

Data from our survey allowed us to understand the market posture of the countries we analysed. Markets with similar characteristics were grouped together to create 4 key groups.

Leaders – Markets where mature ecosystems were driving diverse use-cases and significant consumer uptake.

Movers – Markets with significant momentum behind a shift to API driven data sharing wither regulatory or market driven.

Planners – Markets with progressed regulatory structures and very early stage ecosystems.

Watchers – Markets with early stage regulatory structures but with little infrastructure in place.

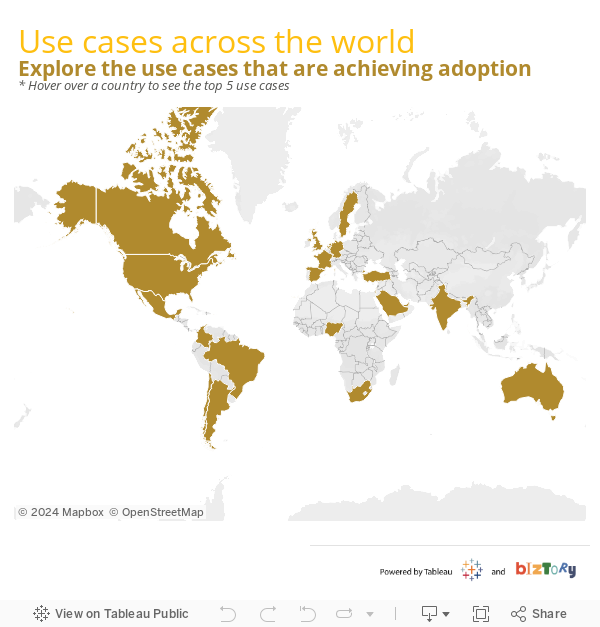

Early-stage markets tended to have a high degree of concentration around one or two use cases, personal finance management (PFM) is particularly prevalent in this group.

More mature ecosytems saw a broader diversity of use-cases, most commonly with lending related use cases coming to the fore.

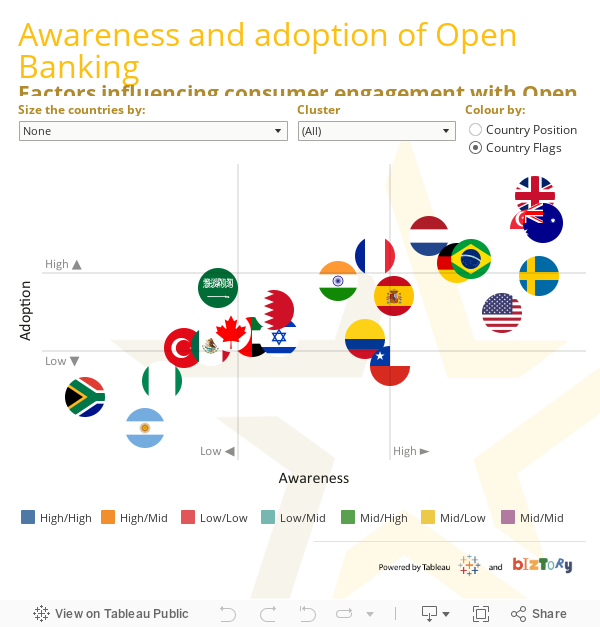

Despite a strong outlier in the case of the US, there is an otherwise strong correlation between markets with mandated adoption of prescriptive standards and the consumer impact of Open Banking.

7 out of the top 10 markets for adoption have taken a mandated approach with 2 of the remaining showing widespread, (voluntary) adoption of similar standards.

Investment in public digital infrastructure also showed a correlation with adoption, particularly around digital ID programs. This will be an area to watch as we progress as much of the digital infrastructure covered in the survey is comparatively early-stage.

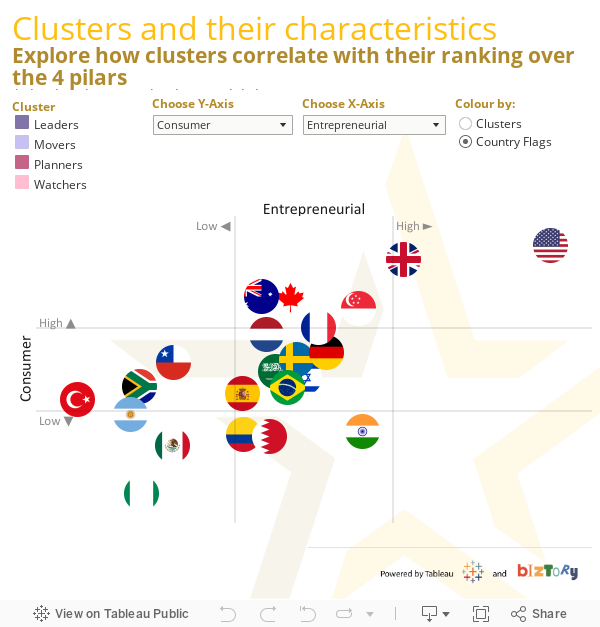

The index methodology is based on tracking market progress against 4 main pillars.

Regulatory environment – covers data around the extent and maturity of the regulation governing Open Banking

Consumer environment – covers data around the state of adoption for digital finance products in market

Ecosystem – Covers the development of a flourishing fintech sector necessary for propagating Open Banking adoption

Entrepreneurial environment – Covers the availability of key components for growing Open Banking businesses (e.g talent, capital, ease of doing business etc…)

We found that, with a relatively small deviation, there was a strong correlation between all 4 categories, with the strongest being between the regulation and consumer pillars.