This is to inform that by clicking on the hyperlink, you will be

leaving

sc.com/sg

and entering a website operated by other parties.

Such links are only provided on our website for the convenience of

the Client and Standard Chartered Bank does not control or endorse

such websites, and is not responsible for their contents.

The use of such website is also subject to the terms of use and

other terms and guidelines, if any, contained within each such

website. In the event that any of the terms contained herein

conflict with the terms of use or other terms and guidelines

contained within any such website, then the terms of use and other

terms and guidelines for such website shall prevail.

Make the most of your SRS account with these strategies

Make the Most of Your SRS Account with These Strategies

Suppose you retire at 65 and need S$4,200 per month for your expenses for the next 20 years, you’ll need a little over S$1 million to sustain your lifestyle post-retirement. That is to say, you’ll have to meet the 1M65 (1 million by 65 years of age) goal for your retirement needs, all the more so if you have dependents to think about.

And what do you have saved up to meet this goal? A study^ shows that Singaporeans often count on their CPF savings to fund their retirement. Yet, CPF is an involuntary scheme meant to only provide you with a very basic retirement income, and the pay-out from it may not be sufficient to meet your requirements.

This is where Supplementary Retirement Scheme (SRS) – an instrument designed to function as an additional retirement planning tool – comes in. With SRS, you not only save more for retirement but also enjoy a number of benefits like tax savings, the ability to choose your investments, and options to withdraw your funds before retirement age.

Here’s a closer look at how you can make the best use of your SRS account. But first, what exactly is SRS?

Part I: Understanding SRS

A voluntary savings scheme^ designed to encourage individuals to save up for retirement over and above their CPF savings, SRS is an account where you can hold your ‘self-contributed’ retirement savings. Contributions to SRS are eligible for tax relief and can be invested in SRS-approved investment products. Before withdrawal, investment-returns are also tax-free.

How Does SRS Help You?

The key advantage of SRS is the tax benefits it offers. Each dollar you contribute to SRS counts towards tax relief^ in the following Year of Assessment. This means that maximum contributions of S$15,300^ for Singaporeans and Permanent Residents, or S$35,700 for foreigners, can be offset from your income in the year you made the contribution, provided it is still within the S$80,000 tax relief cap. The higher your income, the larger the impact on your bottom line. Let’s take a look at an example to understand this better.

In these scenarios, you can see that SRS can be strategically used for tax relief while helping you ensure that your retirement goals are within reach.

Withdrawing from your SRS

Withdrawals from your SRS account^ can be made after the current statutory retirement age of 62 for Singaporeans/PRs or after at least 10 years from the date of your first contribution for foreigners. However, there is the flexibility of early withdrawal at any time, albeit a 5% penalty fee may be imposed and 100% tax on your withdrawal sum. Examples of the types of pre-retirement withdrawals which are not subject to the 5% penalty charge include withdrawals made on medical grounds or in the case of bankruptcy.

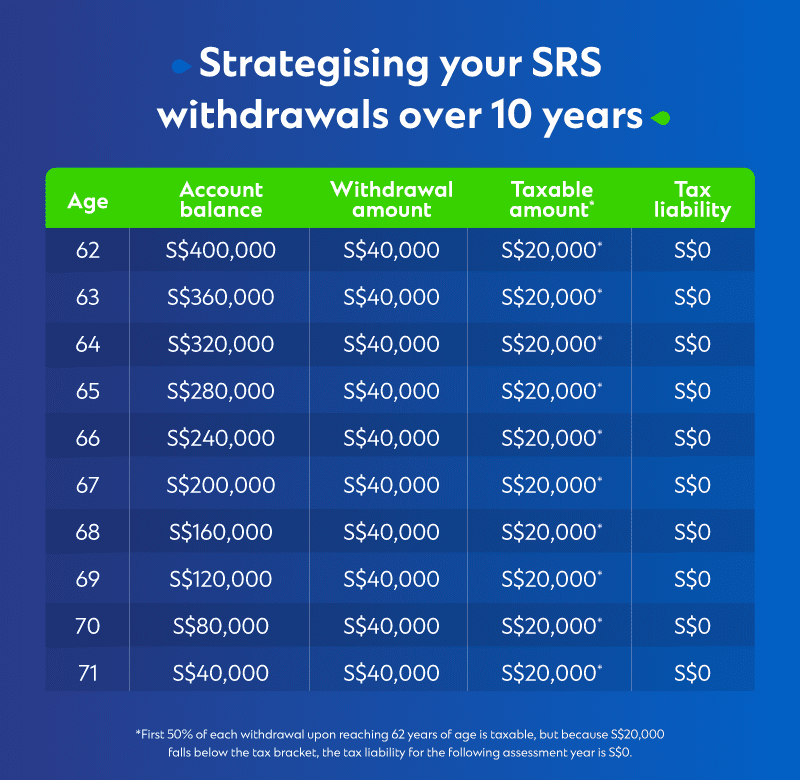

Since withdrawals after the retirement age are taxable at 50% and can be withdrawn over a period of 10 years, you can strategise by making withdrawals only after you have retired and have stopped earning an income. If you have no other source of taxable income, the first $20,000 of your total annual income is tax-exempted. In the perfect scenario, if you withdraw $40,000, only the next $20,000 is taxable (at 50%), but since it falls below the taxable bracket, you effectively have no taxes to pay.

Confusing? Let’s break that down:

*First 50% of each withdrawal upon reaching 62 years of age is taxable, but because S$20,000 falls below the tax bracket, the tax liability for the following assessment year is S$0.

Assuming you withdraw above S$40,000 and have no other source of taxable income, the taxable amount will be as follows:

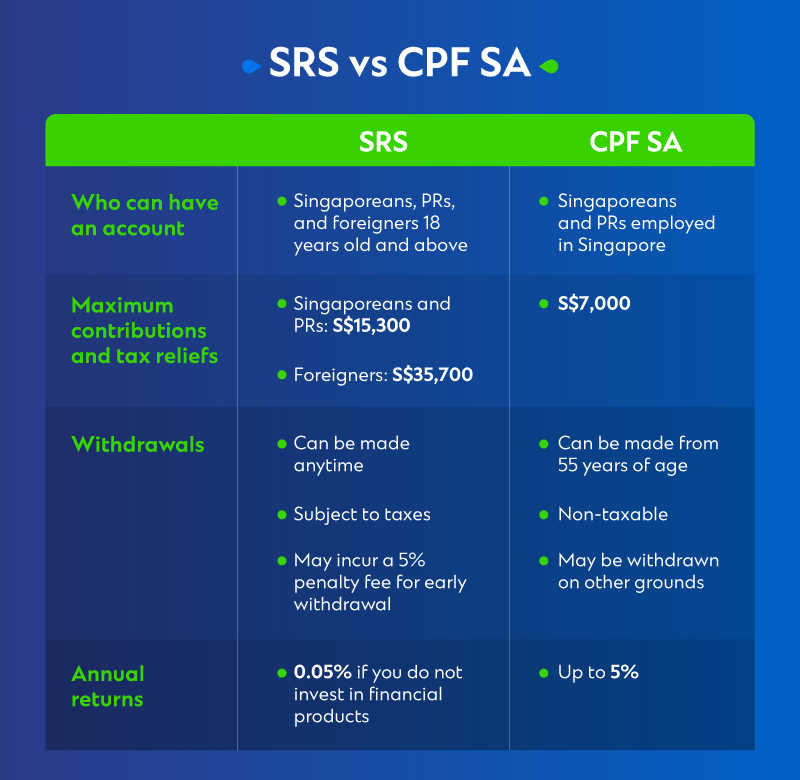

Your monthly CPF contributions go into three accounts^ – one of them being the Special Account (SA) which builds your funds for your retirement and old age. As SRS is also a retirement scheme, let’s take a look at some of the main differences^ between SRS and CPF SA:

With an annual return of 0.05% from SRS, you might be wondering – other than its tax relief benefit, how else can you grow your SRS monies and reap even more benefits?

Part II: Investing Your SRS Contributions

SRS funds can be invested in a wide range of instruments. This works to your advantage because your SRS account offers you the aforementioned interest rate of 0.05% per annum, and your funds are bound to suffer devaluation due to inflation if they are not invested.

It is important to note that while your SRS funds are parked with your preferred SRS operator, you have the choice of diversifying your investment portfolios with other financial institutions in Singapore. That said, the products linked to SRS investments must be government-approved SRS investment products. These include unit trusts, exchange traded funds (ETFs), blue-chip shares, endowment plans, structured deposits, Real Estate Investment Trusts (REITs), Singapore Savings Bonds (SSBs), and Regular Shares Savings (RSS) plans, among others.

Let us take a look at an example to understand the impact of investing your SRS funds:

Based on these scenarios, you would notice the difference between leaving your money in your SRS account to grow, versus investing it. Moreover, choosing the right investment product to suit your needs and risk appetite can make a difference to your accumulated wealth. It is advisable to speak to a Financial Advisor on what investment options are best for you and your hard-earned income.

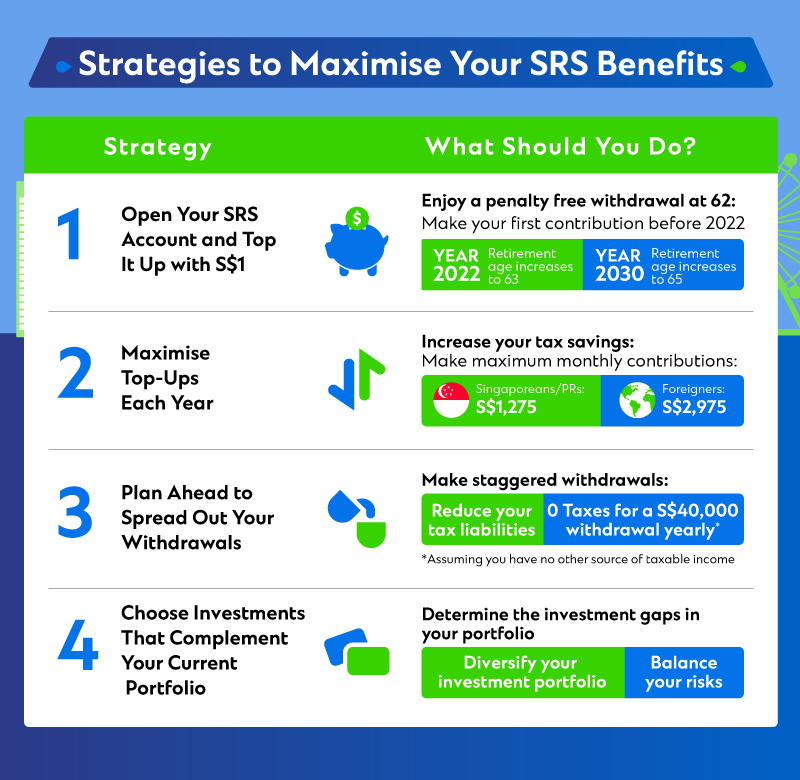

Part III: Maximising your SRS Benefits

From making early contributions to employing the right type of investments, the aim is to get the most out of your SRS account. Here are four strategies that you can consider using to take full advantage of it:

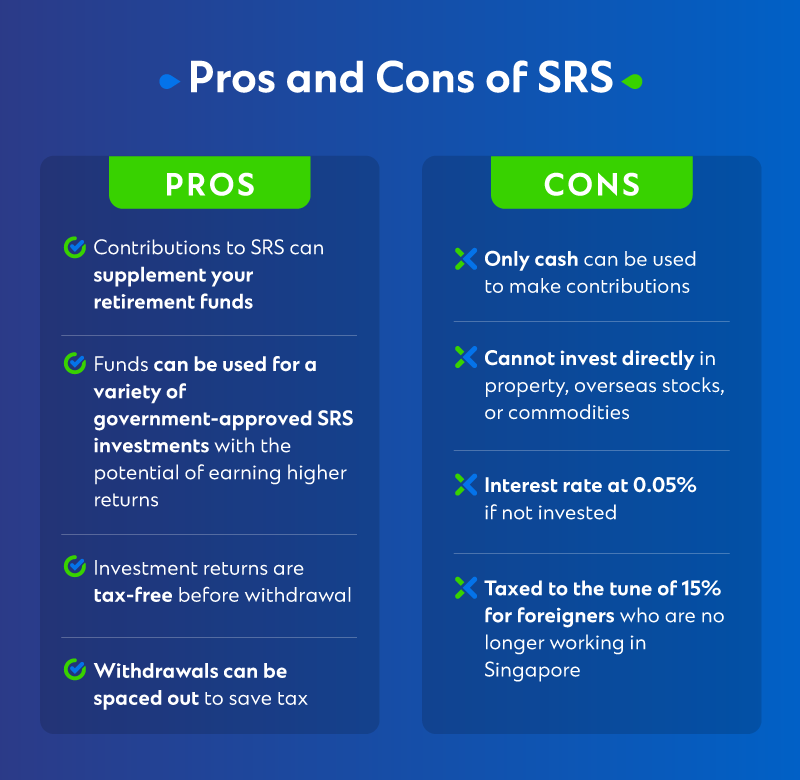

Part IV: Pros and Cons of SRS

Let’s not sugar-coat it – like any products or schemes, there are pros and cons to weigh here as well. Other than benefits like tax savings and the potential to achieve 1M65 with SRS, and the negatives like penalties for most pre-retirement withdrawals, here are some other things to consider when opting to hold your retirement savings in an SRS account:

Maintaining an SRS account is a long-term commitment but offers tax savings and contributes to your retirement fund. You can also use it to step up your game to 2M65 or even 4M65, that is, to aim for 2 million or 4 million in savings by the time you hit 65 years of age.

While your SRS funds are parked with your preferred SRS operator, your SRS investment options are not limited to those provided by them. Explore Standard Chartered’s suite of SRS-approved investment products ranging from unit trusts to endowment plans and more.

Reach out to our Relationship Managers or visit any of our branches for more information on SRS-approved investment products distributed by us and other retirement savings options to start growing your retirement funds, today.

Disclaimer

This article is for general information only and it does not constitute an offer, recommendation or solicitation of an offer to enter into any transaction or adopt any hedging, trading or investment strategy, in relation to any securities or other financial instruments. This article has not been prepared for any particular person or class of persons and does not constitute and should not be construed as investment advice or an investment recommendation. It has been prepared without regard to the specific investment objectives, financial situation or particular needs of any person or class of persons. You should seek advice from a licensed or an exempt financial adviser on the suitability of a product for you, taking into account these factors before making a commitment to purchase any product or invest in an investment. In the event that you choose not to seek advice from a licensed or an exempt financial adviser, you should carefully consider whether the product or service described herein is suitable for you.

You are fully responsible for your investment decision, including whether the investment is suitable for you. The products/services involved are not principal-protected and you may lose all or part of your original investment amount. Standard Chartered Bank (Singapore) Limited will not accept any responsibility or liability of any kind, with respect to the accuracy or completeness of information in this article.

Deposit Insurance Scheme

Singapore dollar deposits of non-bank depositors are insured by the Singapore Deposit Insurance Corporation, for up to S$100,000 in aggregate per depositor per Scheme member by law. For clarity, these investment products are not deposits and do not qualify as an insured deposit under the Singapore Deposit Insurance and Policy Owners’ Protection Schemes Act 2011. Foreign currency deposits, dual currency investments, structured deposits and other investment products are not insured.

The information stated in this article is accurate as at the date of publication.